New Federal Report Shows the Individual Markets Across the Nation Are Stable

California Continues to Benefit From a Healthier Population, Leading to Lower Costs

- The healthier risk mix in California’s individual market results in about 20 percent lower costs compared to the national average, and the other state-based marketplaces’ healthier populations meant 10 percent lower costs.

- Contrary to claims of collapse, the report finds that the risk mix in the individual market was stable in 2016.

- The report highlights how “reinsurance” worked effectively to protect consumers, and the risk-adjustment program moved billions of dollars among carriers to foster a market based on value instead of risk selection.

SACRAMENTO, Calif. — A new report from the Centers for Medicare and Medicaid Services (CMS) on two key premium-stabilization programs in the Patient Protection and Affordable Care Act provides national data that details the stable health mix across the country and the positive impact of the reinsurance program.

The report, “Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2016 Benefit Year,” found that the two programs “functioned smoothly” in 2016 as the Affordable Care Act-compliant market “continued to grow.”

“This report provides hard evidence that contradicts those who would wrongfully claim that individual markets are collapsing,” said Peter V. Lee, executive director of Covered California. “The picture provided by the federal government is one of individual markets that are stable and maintaining a balanced risk mix of those insured, which should inform Congress as it considers what policy steps to take next.”

The report shows the “average risk score” across federal marketplace states, state-based marketplaces and California was nearly the same from 2015 to 2016 (see Figure 1 – Average Risk Score Comparison). More importantly, California’s individual market had a risk profile far better than the national average, which meant health care costs would be nearly 20 percent lower based on health status than the national average.

Further, the report provided important information about which markets are functioning well and how the tools of the current law have worked, including:

- The other state-based marketplaces collectively had a healthier risk mix than the national average, which meant that health care costs in those 10 states would be 10 percent lower than the national average (the analysis excludes Massachusetts and Vermont because risk-score data was not available for these states).

- In summarizing the risk-adjustment program, which is an ongoing feature of the current law, health plans that had “healthier” populations paid a total of nearly $3.6 billion nationally ($392 million in California) to those plans that had less-healthy enrollees.

“California continues to attract a healthy mix of enrollees, and this federal report is further evidence that the individual market in California and across the nation is stable and strong,” said John Bertko, Covered California’s chief actuary. “Generally, the risk profile of a large group gets worse over time, and the fact that across the nation the risk mix stayed constant is clear evidence that relatively healthier individuals are continuing to sign up for insurance.”

Lee identified three key reasons why California and other state-based marketplaces were relatively successful in attracting and keeping a healthier mix of consumers than the national average:

- Covered California and state-based marketplaces appear to be investing proportionately more in marketing and outreach than the federal government, which is responsible for promoting enrollment in the Federally Facilitated Marketplaces.

- State-based marketplaces like California were more likely to convert all health coverage in the individual market into “compliant” plans and created one common risk pool as of 2014.

- California and other states that operate state-based marketplaces were more likely to expand their Medicaid program, which has a positive impact on the health status of the individual market.

In addition to these common factors, Lee noted that in California, health plans offer patient-centered benefit designs, which allow consumers to access a wide variety of care that is not subject to a deductible. That means consumers get more value from their coverage, which is believed to lead to maintaining a better risk mix.

However, Lee says the consumer pool in California and across the nation could be damaged in the face of continued uncertainty on the policy front, in particular regarding the direct payment of the federal cost-sharing reduction subsidy and continued enforcement of the penalty for not having insurance.

“The requirement to have health insurance boosts enrollment, builds a healthier pool of consumers and lowers premiums for everyone,” Lee said. “We are negotiating rates with our carriers right now and the uncertainty about the ongoing payment of the cost-sharing reduction subsidy and enforcement of the mandate risks hurting consumers.”

The report also looked at how “reinsurance” and “risk adjustment” benefit consumers. Similar to the premium-stabilization programs in Medicare Part D, these programs help ensure that health insurance carriers do not avoid enrolling consumers with pre-existing conditions, and they protect carriers that enroll a disproportionately sicker pool of consumers.

The report states, “Both the transitional reinsurance program and the permanent risk adjustment program are working as intended in compensating plans that enrolled higher-risk individuals, thereby protecting issuers against adverse selection within a market within a state and supporting them in offering products that serve all types of consumers.”

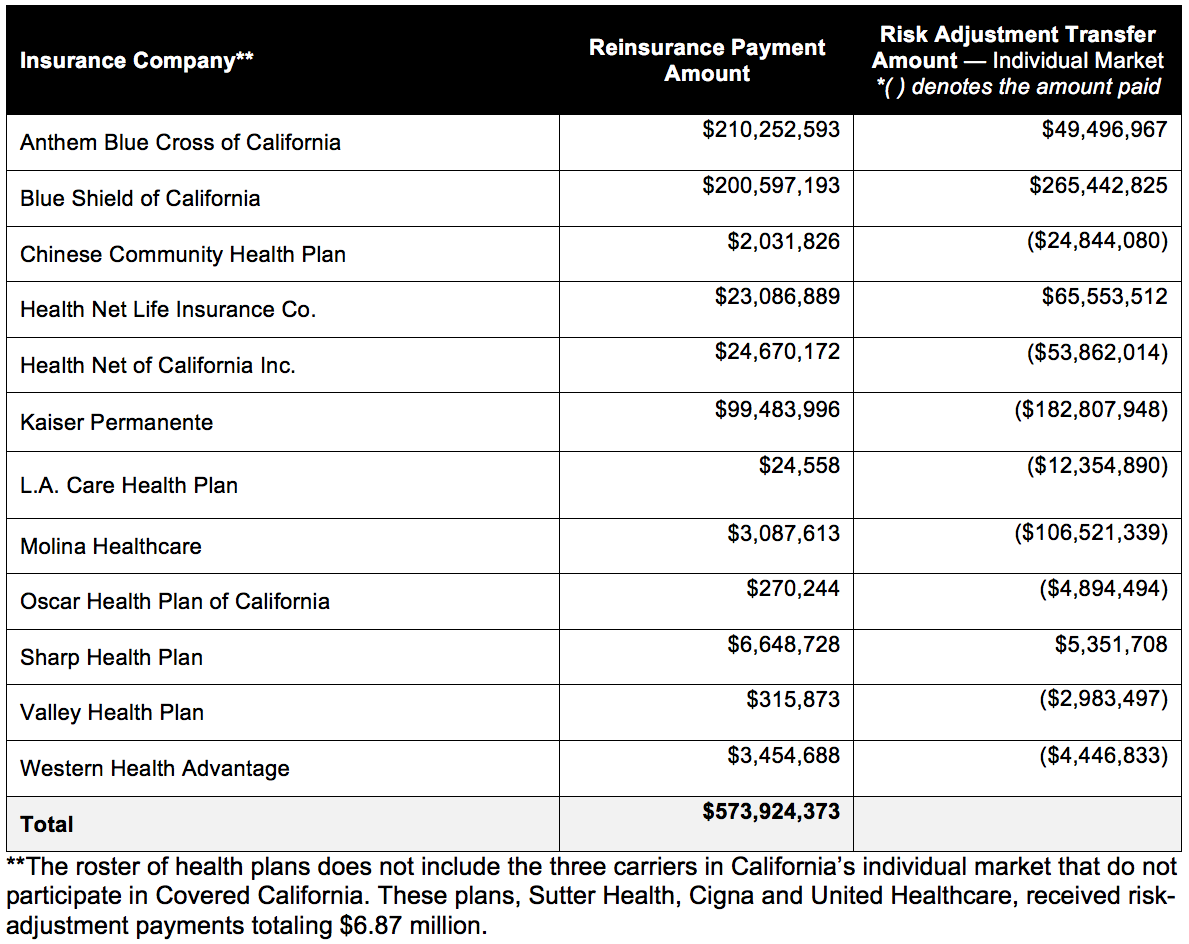

In 2016, health insurance companies within California’s individual market received more than $573 million in reinsurance payments, which had the direct effect of lowering premiums for all consumers. The money for reinsurance came from a fee on all private health insurance coverage (in the individual, small-employer, large-employer insured and large-employer self-insured markets), and the risk-adjustment payments are from the health insurance companies themselves and do not include taxpayer dollars. This year, 2016, marked the final year of the reinsurance program.

“The risk-adjustment mechanism is working to move insurers to compete on providing better care at a better price, rather than being rewarded for avoiding sicker people,” said Lee.

The table below shows the amounts each of California’s carriers received through reinsurance and how much they either paid or received through risk adjustment.

The full CMS report can be viewed here: https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/Downloads/Summary-Reinsurance-Payments-Risk-2016.pdf.

About Covered California

Covered California is the state’s health insurance marketplace, where Californians can find affordable, high-quality insurance from top insurance companies. Covered California is the only place where individuals who qualify can get financial assistance on a sliding scale to reduce premium costs. Consumers can then compare health insurance plans and choose the plan that works best for their health needs and budget. Depending on their income, some consumers may qualify for the low-cost or no-cost Medi-Cal program.

Covered California is an independent part of the state government whose job is to make the health insurance marketplace work for California’s consumers. It is overseen by a five-member board appointed by the governor and the legislature. For more information about Covered California, please visit www.CoveredCA.com.