New Analysis Finds Leading State-Based Marketplaces Have Performed Well, and Highlights the Impact of the Federal Mandate Penalty Removal

Tweet This

- The report examines the impact that federal and state actions have had on state-based marketplaces and the federally facilitated marketplace (FFM).

- Cumulative premium increases in California, Massachusetts and Washington are less than half of the increases seen in FFM states, but 2019 premium increases spiked in California and Washington compared to Massachusetts, which continued its state-based penalty.

WASHINGTON D.C. — A new report highlights the benefits of state-based exchanges, particularly in the areas of controlling premium costs and attracting new enrollment. The report, which was produced by Covered California, the Massachusetts Health Connector and the Washington Health Benefit Exchange, found that premiums in these states were less than half of what consumers saw in the 39 states that relied on the federally facilitated marketplace (FFM) between 2014 and 2019.

“The lesson is striking: Consumers are the big winners when marketplaces use all the tools of the Affordable Care Act,” said Covered California Executive Director Peter V. Lee. “The policies underway in these three states are easily transferable, and if applied to the federal marketplace, taxpayers would save billions of dollars in subsidies, and middle-class Americans would benefit from much lower premiums.”

The joint report examined how state and federal actions affected premiums and new enrollment.

State-Based Marketplaces Controlled Premium Growth

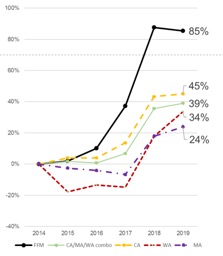

The report examined the cost of coverage by comparing the average benchmark premium in three states and the FFM between 2014 and 2019. The weighted average increase in California, Massachusetts and Washington was 39 percent, compared to the 85 percent increase in FFM states.

Figure1: Average Benchmark Premium Growth by Percentage, Compared to 2014

In addition, the report also found if the FFM states had experienced the same lower premium growth seen in the three states, the federal government could have saved roughly $35 billion in lower subsidy payments between 2014 and 2018.

While the report did not quantify the increased costs paid by unsubsidized consumers in FFM states, they would have saved substantially and been less likely to have been priced out of coverage.

State-Based Marketplaces Peformed Better at Enrolling New Consumers

Source: Kaiser Family Foundation. https://www.kff.org/health-reform/state-indicator/marketplace-average-benchmark-premiums/. Estimates of cost savings use benchmark premium data. FFM includes SBM-FP states.

The report also examined the impact on new enrollment of recent federal decisions on marketing and outreach and the elimination of the individual mandate penalty.

During the final days of open enrollment for the 2017 plan year, the federal administration began a series of cuts to marketing and outreach on behalf of FFM states. These cuts have been deepened and maintained, resulting in a significant reduction in new enrollment in states served by the federal marketplace. The decrease in new enrollment likely means a less-healthy consumer pool, which would lead to the larger premium increases seen above.

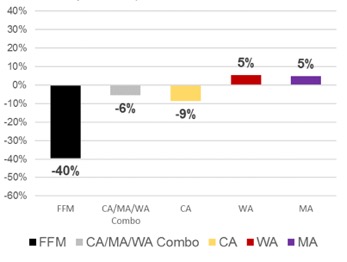

From 2016 to 2018, the 39 FFM states saw the number of new enrollees drop from 4 million to 2.5 million, a decrease of 40 percent. By contrast, new enrollment in California, Massachusetts and Washington — states that control their own marketing and outreach — remained relatively stable (see Figure 2: New Enrollment Growth by Marketplace, Comparing 2016 to 2018).

“State-based marketplaces know that health insurance is a product that needs to be actively sold to consumers, and getting the word out is a proven way to promote enrollment,” said Pam MacEwan, chief executive officer of the Washington Health Benefit Exchange. “Enrolling more people means a healthier risk pool, which lowers premiums and saves money for everyone in the individual market.”

Figure 2: New Enrollment Growth by Marketplace, Comparing 2016 to 2018

Clear Indication of the Critical Role of the Individual Mandate Penalty in Promoting Enrollment

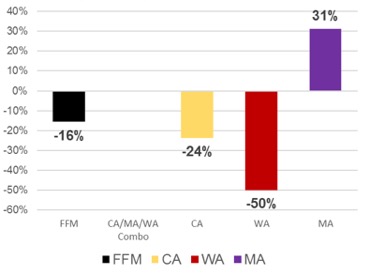

The open-enrollment period that just concluded for the 2019 coverage year marked the first time the marketplaces would operate without a federal individual mandate penalty, which was zeroed out through the Tax Cuts and Jobs Act of 2017 and signed into law by the president. During the most recent open-enrollment period, new enrollment in FFM states dropped an additional 16 percent — on top of the already large drop of 40 percent in the prior two years. California and Washington also experienced steep declines in the number of new enrollees signing up for coverage. However, Massachusetts — which kept a state-level mandate penalty — saw new enrollment increase by 31 percent (see Figure 3: New Enrollment Growth by Marketplace, Comparing 2018 to 2019).

Figure 3: New Enrollment Growth by Marketplace, Comparing 2018 to 2019

“The individual mandate in Massachusetts has proven to be an effective part of our effort to provide access to affordable coverage to everyone,” said Louis Gutierrez, executive director of the Massachusetts Health Connector. “Our experience shows that a mandate that provides incentive to participate, while also delivering important protections and benefits to consumers, plays a vital role not only in people getting covered, but also staying covered.”

Other marketplaces have also instituted a penalty, such as New Jersey and the District of Columbia. While critics may point to lower new enrollment in New Jersey as proof that a penalty is not effective, Lee says that is not the case. “The penalty works, and to solely highlight New Jersey — which had a penalty in place, but also had its marketing and outreach efforts undercut — is not a reasonable comparison.”

“While Washington kept premium increases in the early years of the Affordable Care Act to low single digits, the past three years have seen big increases due to federal policy changes that continue to bring uncertainty to the market, including the zeroing of the individual mandate penalty,” said MacEwan. “In particular, 2019 saw an almost 14 percent premium increase. These premium increases are having a large negative impact on the many Washington consumers who do not benefit from a subsidy.”

The release of the report comes on the same day that leaders of the California and Massachusetts marketplaces appeared before the Health Subcommittee of the U.S.

House Committee on Energy and Commerce. View the hearing on “Strengthening Our Health Care System: Legislation to Lower Consumer Costs and Expand Access.”

Read the testimonies of representatives from California and Massachusetts at the committee hearing.

About Covered California

Covered California is the state’s health insurance marketplace, where Californians can find affordable, high-quality insurance from top insurance companies. Covered California is the only place where individuals who qualify can get financial assistance on a sliding scale to reduce premium costs. Consumers can then compare health insurance plans and choose the plan that works best for their health needs and budget. Depending on their income, some consumers may qualify for the low-cost or no-cost Medi-Cal program.

Covered California is an independent part of the state government whose job is to make the health insurance marketplace work for California’s consumers. It is overseen by a five-member board appointed by the governor and the Legislature. For more information about Covered California, please visit www.CoveredCA.com.

Covered California can be contacted at media@covered.ca.gov or (916) 206-7777.

About the Massachusetts Health Connector

The Massachusetts Health Connector is the Commonwealth’s health insurance exchange, and currently provides health or dental insurance to more than 300,000 people. Individuals and small businesses can search for and purchase high-quality, commercial coverage, while reaping the health and financial benefits of being covered. Individuals and small businesses can find health insurance options at www.MAhealthconnector.com.

For information on the Massachusetts Health Connector, contact Jason Lefferts, director of Communications and Media Relations, at (617) 933-3141.

About theWashington Health Benefit Exchange

The Washington Health Benefit Exchange, or Washington Healthplanfinder, is an online marketplace for individuals and families in Washington to compare and enroll in health insurance coverage and gain access to tax credits, reduced cost-sharing and public programs such as Medicaid. The next open-enrollment period in Washington begins on Nov. 1.

The Washington Health Benefit Exchange can be reached at ben.spradling@wahbexchange.org.